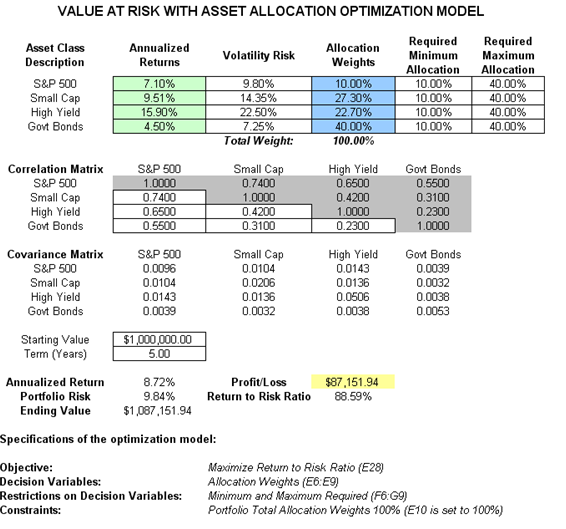

Now that we understand the concepts of optimized portfolios, let us see what the effects are on computed economic capital through the use of a correlated portfolio VaR. This model uses Monte Carlo simulation and optimization routines in Risk Simulator to minimize the VaR of a portfolio of assets (Figure 2.18). The file used is Value at Risk – Optimized and Simulated Portfolio VaR that is accessible via Modeling Toolkit | Value at Risk | Optimized and Simulated Portfolio VaR. In this example model, we intentionally used only 4 asset classes to illustrate the effects of an optimized portfolio, whereas in real life, we can extend this to cover a multitude of asset classes and business lines. In addition, we now illustrate the use of a left-tail VaR, as opposed to a right-tail VaR, but the concepts are similar.

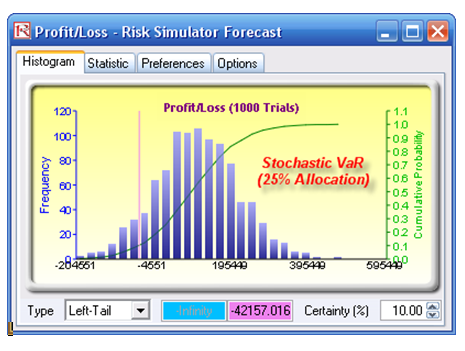

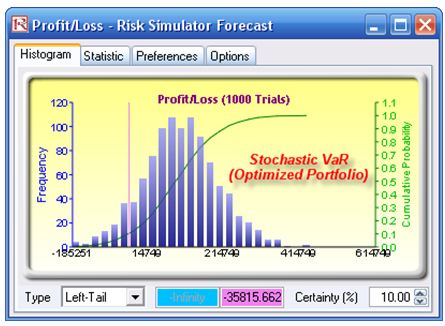

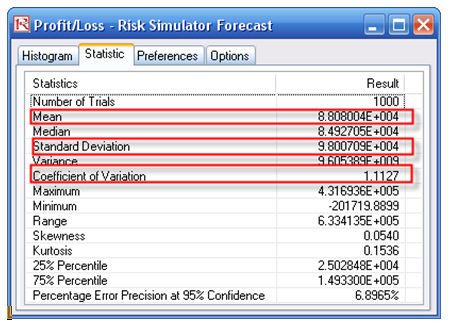

First, simulation is used to determine the 90% left-tail VaR (this means that there is a 10% chance that losses will exceed this VaR for a specified holding period). With an equal allocation of 25% across the 4 asset classes, the VaR is determined using simulation (Figure 2.19). The annualized returns are uncertain and, hence, simulated. The VaR is then read off the forecast chart. Then, optimization is run to find the best portfolio subject to the 100% allocation across the 4 projects that will maximize the portfolio’s bang-for-the-buck (returns to risk ratio). The resulting optimized portfolio is then simulated once again and the new VaR is obtained (Figure 2.20). The VaR of this optimized portfolio is a lot less than the not optimized portfolio. That is, the expected loss is $35.8M instead of $42.2M, which means that the bank will have a lower required economic capital if the portfolio of holdings is first optimized.

Figure 2.18: Computing Value at Risk (VaR) with Simulation

Figure 2.19: Unoptimized Value at Risk

Figure 2.20: Optimal Portfolio’s Value at Risk through Optimization and Simulation