File Name: Debt Analysis – Vasicek Debt Option Valuation

Location: Modeling Toolkit | Debt Analysis | Vasicek Debt Option Valuation

Brief Description: Applies the Vasicek model of debt options assuming that interest rates are stochastic, volatile, and mean-reverting

Requirements: Modeling Toolkit, Risk Simulator

Modeling Toolkit Functions Used: MTBondVasicekBondCallOption, MTBondVasicekBondPutOption

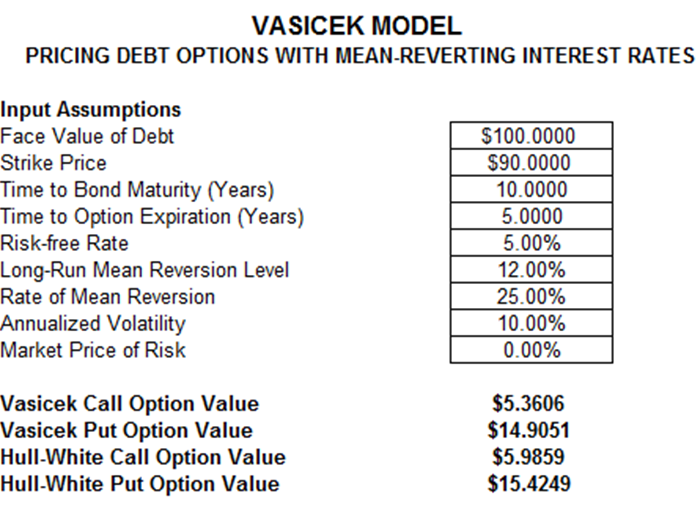

This is the Vasicek model on bond or debt options, where the underlying debt issue changes in value based on the level of prevailing interest rates; that is, the interest rates have a mean-reverting tendency where the interest rate at any future period approaches a long-run mean interest rate with a rate of reversion and volatility around this reversion trend (Figure 21.1). Both options are European and can be executed only at expiration. To determine other types of options such as American and Bermudan options, use the Modeling Toolkit’s Options on Debt modules to build lattices on mean-reverting interest rates and their respective option values.

A few interesting behaviors can be determined from this model. Typically, a bond call option will have a lower value if the long-run mean interest rate is higher than the current spot risk-free rate and if the rate of reversion is high (this means that the spot interest rates reverts to this long-run rate quickly). The inverse situation is also true, where the bond call option value is higher if the long-run rate is lower than the spot rate and if the reversion rate is high. The opposite effects apply to the bond put option. Nonetheless, the reversion effect will be overshadowed by a high volatility of interest rates. Finally, at negligible maturities and interest rates (e.g., bond maturity of 0.01, option maturity of 0.001, spot risk-free rate of 0.001) the bond option values revert to the intrinsic value or Face Value – Strike for bond call option, and Strike – Face Value for put option.

There are also another two models for solving bond call and put options available through the functions:

MTBondHullWhiteBondCallOption

MTBondHullWhiteBondPutOption

These two Hull-White models are slightly different in that they do not require a long-run interest rate. Rather, just the reversion rate will suffice. If we calibrate the long-run rate in the Vasicek model carefully, we will obtain the same results as the Hull-White model. Typically, the Vasicek model is simpler to use.

Figure 21.1: Vasicek model of pricing debt options and yield with mean-reverting rates