File Name: Exotic Options – Lookback with Floating Strike

Location: Modeling Toolkit | Exotic Options | Lookback Floating Strike

Brief Description: Computes the value of an option where the strike price is not fixed but floating, and the value at expiration is based on the value of the underlying asset’s maximum and minimum values during the option’s lifetime as the purchase or sale price

Requirements: Modeling Toolkit

Modeling Toolkit Functions Used: MTFloatingStrikeLookbackCallonMin, MTFloatingStrikeLookbackPutonMax

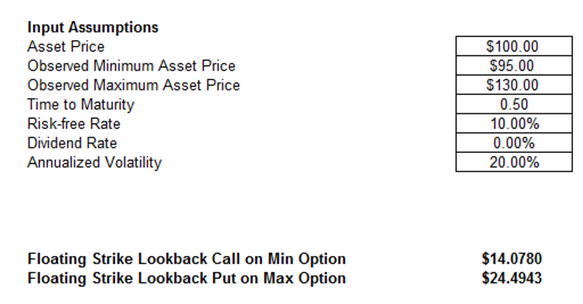

In a Floating Strike Option with Lookback Feature, the strike price is floating. At expiration, the payoff on the call option is being able to purchase the underlying asset at the minimum observed price during the life of the option. Conversely, the put will allow the option holder to sell at the maximum observed asset price during the life of the option (Figure 64.1).

Figure 64.1: Lookback options with floating strike