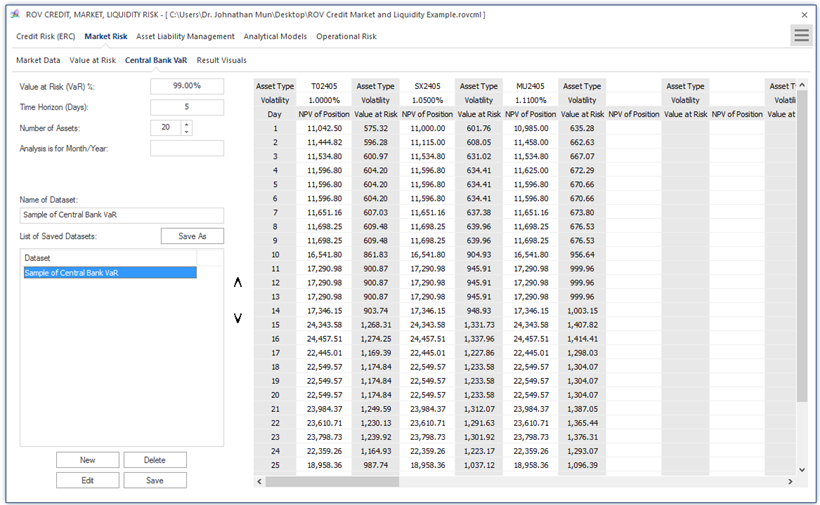

Figure 1.5 illustrates the Central Bank VaR method and results in computing VaR based on user settings (e.g., the VaR percentile, time horizon of the holding period in days, number of assets to analyze, and the period of the analysis) and the assets’ historical data. The VaR computations are based on the same approach as previously described, and the inputs, settings, and results can be saved for future retrieval.

Figure 1.5: Market Central Bank VaR