File Name: Exotic Options – Commodity Options

Location: Modeling Toolkit | Exotic Options | Commodity Options

Brief Description: Models and values a commodity option where the commodity’s spot and future values are used to value the option, while the forward rates and convenience yields are assumed to be mean-reverting and volatile

Requirements: Modeling Toolkit

Modeling Toolkit Functions Used: MTCommodityCallOptionModel, MTCommodityPutOptionModel

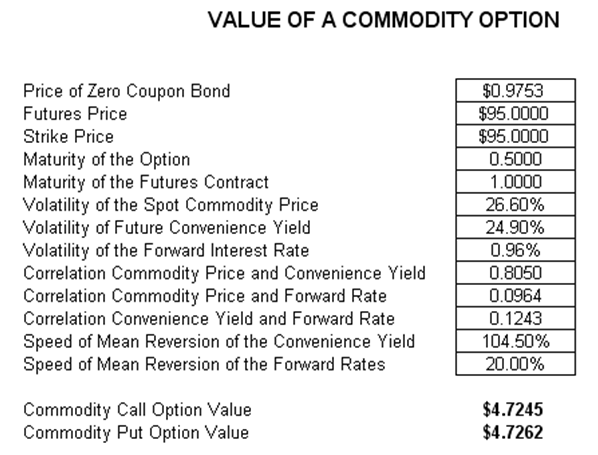

This model computes the values of commodity-based European call and put options, where the convenience yield and forward rates are assumed to be mean-reverting, and each has its own volatilities and cross-correlations. This is a complex multifactor model with inter-relationships among all variables. An example of valuing a commodity option is provided in Figure 43.1.

Figure 43.1: Computing the commodity option