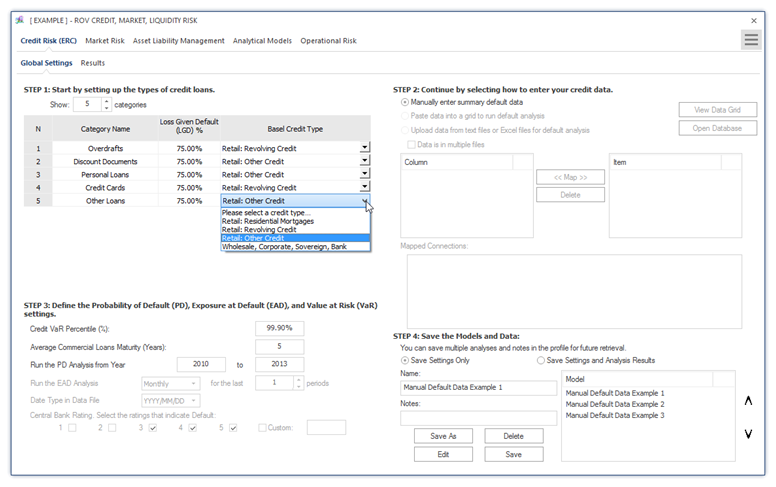

Figure 1.1 illustrates the ROV PEAT software’s ALM-CMOL module for Credit Risk—Economic Regulatory Capital (ERC) Global Settings tab. This current analysis is performed on credit issues such as loans, credit lines, and debt at the commercial, retail, or personal levels. To get started with the utility, existing files can be opened or saved, or a default sample model can be retrieved from the menu. However, to follow along, we recommend opening the default example (click on the menu icon on the top right corner of the software, then select Load Example).

The number of categories of loans and credit types can be set as well as the loan or credit category names, a Loss Given Default (LGD) value in percent, and the Basel credit type (residential mortgages, revolving credit, other miscellaneous credit, or wholesale corporate and sovereign debt). Each credit type has its required Basel III/IV model that is public knowledge, and the software uses the prescribed models per Basel regulations. Further, historical data can be manually entered by the user into the utility or via existing databases and data files. Such data files may be large and, hence, stored either in a single file or multiple data files where each file’s contents can be mapped to the list of required variables (e.g., credit issue date, customer information, product type or segment, Central Bank ratings, amount of the debt or loan, interest payment, principal payment, last payment date, and other ancillary information the bank or financial services firm has access to) for the analysis, and the successfully mapped connections are displayed. Additional information such as the required VaR percentiles, average life of a commercial loan, and historical data period on which to run the data files to obtain the Probability of Default (PD) is entered. Next, the Exposure at Default (EAD) analysis periodicity is selected as is the date type and the Central Bank ratings. Different Central Banks in different nations tend to have similar credit ratings but the software allows for flexibility in choosing the relevant rating scheme (i.e., Level 1 may indicate on-time payment of an existing loan whereas Level 3 may indicate a late payment of over 90 days, which, therefore, constitutes a default). All these inputs and settings can be saved either as stand-alone settings and data or including the results. Users would enter a unique name and notes and save the current settings (previously saved models and settings can be retrieved, edited, or deleted; a new model can be created; or an existing model can be duplicated). The saved models are listed and can be rearranged according to the user’s preference.

Figure 1.1: Credit Risk Settings