File Name: Exotic Options – Extreme Spreads

Location: Modeling Toolkit | Exotic Options | Extreme Spreads

Brief Description: Computes extreme spread option values, where the vehicle is divided into two segments, and the option pays off the difference between the extreme values (min or max) of the asset during the two time segments

Requirements: Modeling Toolkit

Modeling Toolkit Functions Used: MTExtremeSpreadCallOption, MTExtremeSpreadPutOption, MTExtremeSpreadReverseCallOption, MTExtremeSpreadReversePutOption

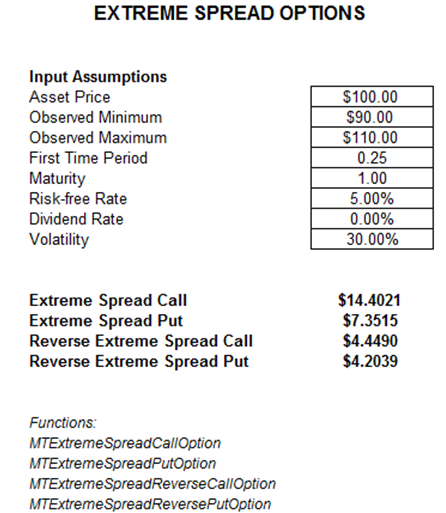

Extreme Spread Options (Figure 48.1) have their maturities divided into two segments, starting from time zero to the First Time Period (first segment) and from the First Time Period to Maturity (second segment). An extreme spread call option pays the difference between the maximum asset value from the second segment and the maximum value of the first segment. Conversely, the put pays the difference between the minimum of the second segment’s asset value and the minimum of the first segment’s asset value. A reverse call pays the minimum from the first less the minimum of the second segment, whereas a reverse put pays the maximum of the first less the maximum of the second segments.

Figure 48.1: Extreme spreads options