File Name: Yield Curve – Forward Rates from Spot Rates

Location: Modeling Toolkit | Yield Curve | Forward Rates from Spot Rates

Brief Description: This is a bootstrap model used to determine the implied forward rate given two spot rates

Requirements: Modeling Toolkit, Risk Simulator

Modeling Toolkit Function Used: MTForwardRate

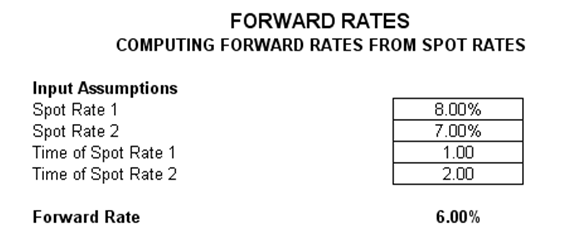

Given two spot rates (from Year 0 to some future time periods), you can determine the implied forward rate between these two time periods. For instance, if the spot rate from Year 0 to Year 1 is 8%, and the spot rate from Year 0 to Year 2 is 7% (both yields are known currently), the implied forward rate from Year 1 to Year 2 (that will occur based on current expectations) is 6%. This is simplified by using the MTForwardRate function in Modeling Toolkit (Figure 2.34).

Figure 2.34: Forward Rate Extrapolation