File Name: Exotic Options – Barrier Options

Location: Modeling Toolkit | Exotic Options | Barrier Options

Brief Description: Values various types of barrier options such as up and in, down and in, up and out, and down and out call and put options

Requirements: Modeling Toolkit

Modeling Toolkit Functions Used: MTBarrierDownandInCall, MTBarrierUpandInCall, MTBarrierDownandInPut, MTBarrierUpandInPut, MTBarrierDownandOutCall, MTBarrierUpandOutCall, MTBarrierDownandOutPut, MTBarrierUpandOutPut

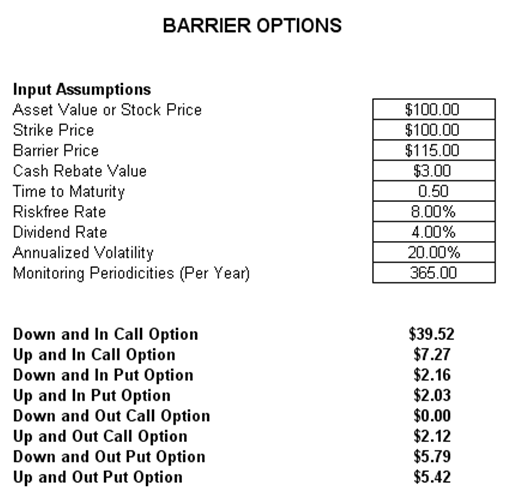

Barrier options become valuable or get knocked in the money only if a barrier (upper or lower barrier) is breached (or not), and the payout is in the form of the option on the underlying asset. Sometimes, as remuneration for the risk of not being knocked in, a specified cash rebate is paid at the end of the instrument’s maturity (at expiration) assuming that the option has not been knocked in.

As an example, in an Up and In Call option, the instrument pays the specified cash amount at expiration if and only if the asset value does not breach the upper barrier (the asset value does not go above the upper barrier), providing the holder of the instrument with a safety net or cash insurance. However, if the asset breaches the upper barrier, the option gets knocked in and becomes a live option. An Up and Out option is live only as long as the asset does not breach the upper barrier, and so forth. Monitoring Periodicities means how often during the life of the option the asset or stock value will be monitored to see if it breaches a barrier. As an example, entering 12 implies monthly monitoring, 52 means weekly monitoring, 252 indicates monitoring for daily trading, 365 means monitoring daily, and 1,000,000 means continuous monitoring.

In general, barrier options limit the potential of a regular option’s profits and hence cost less than regular options without barriers. For instance, in Figure 38.1, if we assume no cash rebates, a Generalized Black-Scholes call option returns $6.50 as opposed to $5.33 for a barrier option (up and in barrier set at $115 with a stock price and strike price value of $100). This is because the call option will only be knocked in if the stock price goes above this $115 barrier, thereby reducing the regular option’s profits between $100 and $115. This reduction effect is even more pronounced in the up-and-out call option, where all the significant upside profits (above the $115 barrier) are completely truncated.

Figure 38.1: Computing barrier options