File Names: Real Options – Strategic Cases – Switching Option’s Strategy A; Real Options – Strategic Cases – Switching Option’s Strategy B

Location: Modeling Toolkit | Real Options Models

Brief Description: Frames and values a real options application of the ability to switch use when the underlying project is filled with risk and uncertainty

Requirements: Modeling Toolkit, Real Options SLS

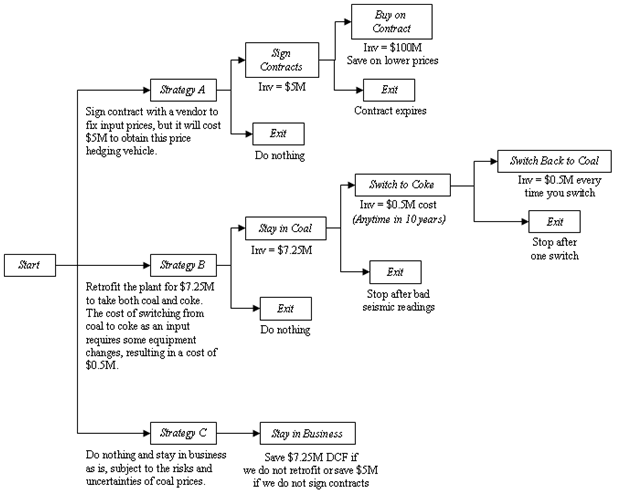

This strategic case is a switching option (an electric generating plant can be retrofitted to take both coke and coal as inputs, as opposed to the current situation where only one type of input can be used) and can be summarized in the strategy tree shown in Figure 197.1.

Figure 197.1: Strategy tree for switching options

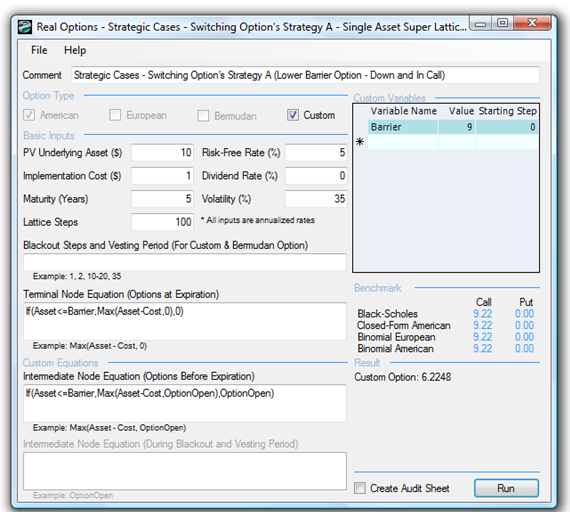

In Strategy A, signing a contract where it comes into play only when prices hit a lower level is a Lower Down and In Barrier Call Option. The PV asset value is the current NPV staying on course, and the lower barrier is the NPV value that is obtained given the lower price level where the contract is executed. Signing the contract is worth more than Strategy B’s ability to switch; hence, Strategy A should be executed. Besides, this is a lot less expensive than retrofitting the plant to take different inputs. The total strategic value is positive as the option value of this contract is $6.22M (Figure 197.2) but the cost of executing the contract to buy the option is $5M.

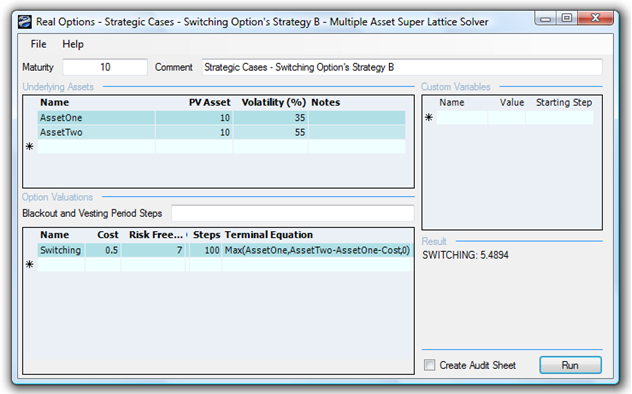

In Strategy B, the ability to switch back and forth has some value even if both input fuels are at the same price currently. In fact, the NPV shows that there is no value in the ability to switch. If using coal right now has an NPV of $10M and coke also has an NPV of $10M because their price levels are currently the same, then the act of switching incurs a $0.5M cost, and switching now yields an NPV of –$0.50M. Obviously, then, the ability to switch is useless in an NPV paradigm. However, in a real options paradigm, having the ability to switch but not doing it right now is worth a lot. For instance, coal and coke have different volatilities in prices and may or may not be correlated (a negative correlation increases the switching option’s value as the new input acts like a hedging vehicle). The price movements of both inputs are highly volatile and there is a chance that the first input’s prices are higher than the second inputs such that switching becomes optimal. The strategic value yields $5.49M (regardless if it is switching from coal with 35% volatility to coke with 55%, or vice versa). However, the cost of getting this option (retrofitting the plant) is $7.25M, so the total strategic value is negative, making this strategy not optimal (Figure 197.3).

Figure 197.2: Switching option Strategy A

Figure 197.3: Switching option Strategy B