File Name: Risk Hedging – Hedging Foreign Exchange Exposure

Brief Description: This model illustrates how to use Risk Simulator for simulating foreign exchange rates to determine the value of a hedged currency option position

Requirements: Modeling Toolkit, Risk Simulator

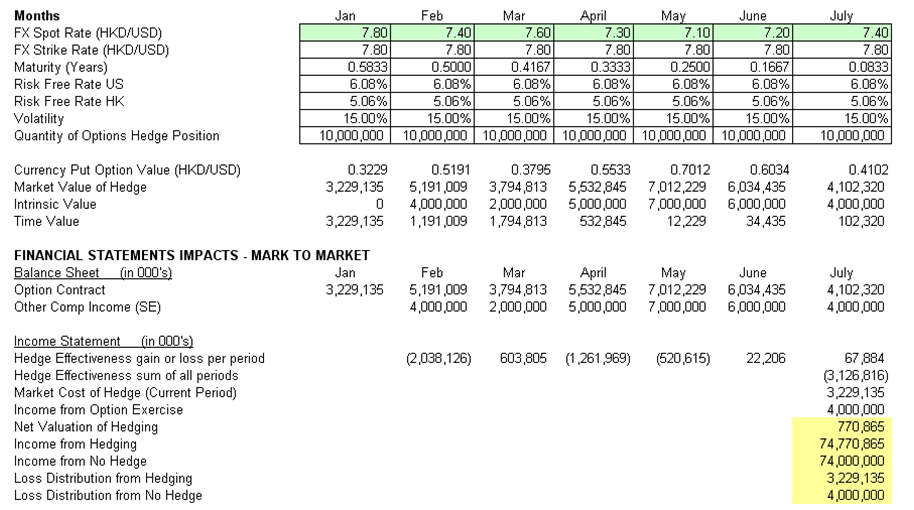

This model is used to simulate possible foreign exchange spot and future prices and the effects on the cash flow statement of a company under a freely floating exchange rate versus using currency options to hedge the foreign exchange exposure (Figure 2.26).

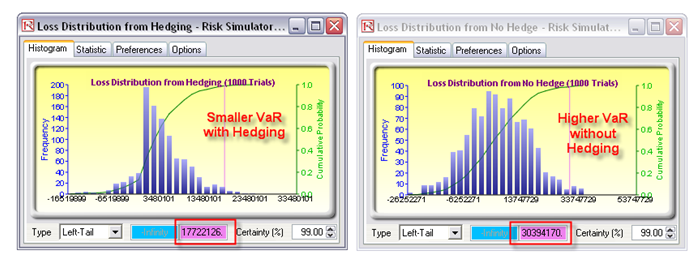

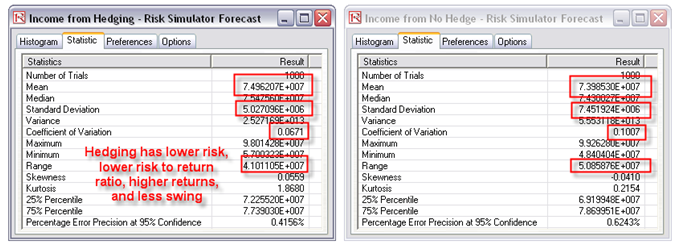

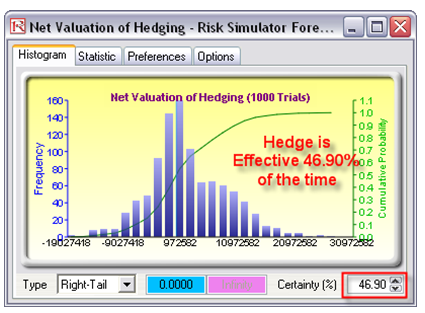

Figure 2.27 shows the effects of the Value at Risk (VaR) of a hedged versus unhedged position. Clearly, the right-tailed VaR of the loss distribution is higher without the currency options hedge. Figure 2.27 shows that there is a lower risk, lower risk to returns ratio, higher returns, and less swing in the outcomes of a currency-hedged position than an exposed position, with Figure 2.28 showing the simulated forecast statistics of the loss distribution. Finally, Figure 2.29 shows the hedging effectiveness, that is, how often the hedge is in the money and becomes usable.

![]()

Figure 2.26: Hedging Currency Exposures with Currency Options

Figure 2.27: Values at Risk (VaR) of Hedged Versus Unhedged Positions

Figure 2.28: Forecast Statistics of the Loss Distribution

Figure 2.29: Hedging Effectiveness