File Name: Exotic Options – Trading Day Corrections

Location: Modeling Toolkit | Exotic Options | Trading Day Corrections

Brief Description: Computes the value of plain vanilla call and put options corrected for the number of trading days and calendar days left in their maturity

Requirements: Modeling Toolkit

Modeling Toolkit Functions Used: MTTradingDayAdjustedCall, MTTradingDayAdjustedPut, MTGeneralizedBlackScholesCall, MTGeneralizedBlackScholesPut

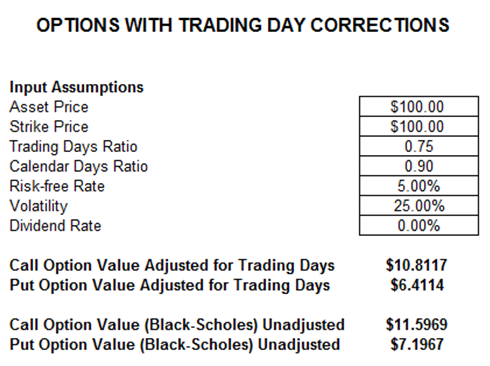

An Option with a Trading-Day Correction uses a typical option and corrects it for the varying volatilities (Figure 74.1). Specifically, volatility tends to be higher on trading days than on nontrading days. The Trading Days Ratio is simply the number of trading days left until maturity divided by the total number of trading days per year (typically between 250 and 252). The Calendar Days Ratio is the number of calendar days left until maturity divided by the total number of days per year (365).

Typically, with the adjustments, the option value is lower. In addition, if the trading-days ratio and calendar-days ratio are identical, the result of the adjustment is zero and the option value reverts back to the generalized Black-Scholes results. This is because the number of days left is assumed to be all fully trading.

Figure 74.1: Options with trading-day corrections