As with any other Basel-defined risk, key risk indicators or KRIs are constructed based on the inputs and results of the modeling tool and can be duly monitored and reported in line with the IMMM process. Liquidity and interest-rate risk are usually managed together in a function called ALM, short for Asset Liability Management. These two risks are closely intertwined since liquidity risk monitors the availability of liquid funds to confront disbursement requirements (usually in three time-horizons: immediate and intraday, short-term structure, and long-term structure), while interest-rate risk measures the impact of the difference in maturities, or duration, for assets and liabilities.

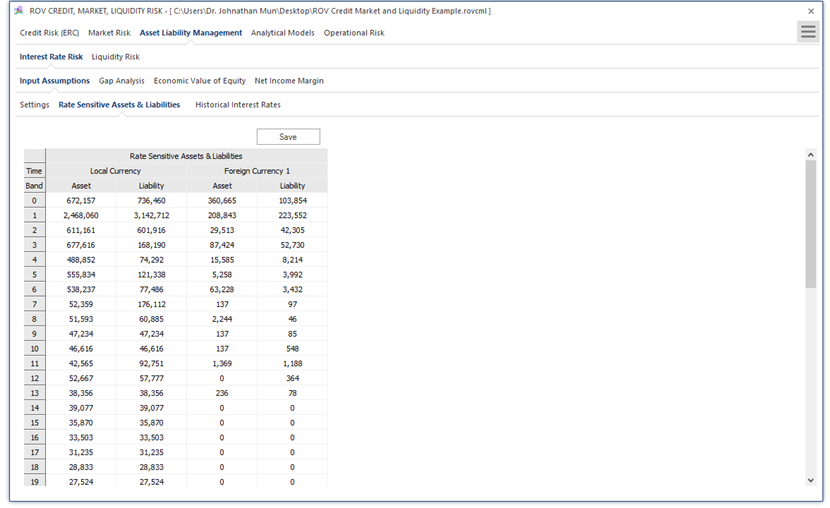

Figure 1.6 illustrates the PEAT utility’s ALM-CMOL module for Asset Liability Management—Interest Rate Risk’s Input Assumptions and general Settings tab. This segment represents the analysis of Asset Liability Management (ALM) computations. ALM is the practice of managing risks that arise due to mismatches between the maturities of assets and liabilities. It is about offering solutions to mitigate or hedge the risks arising from the interaction of assets and liabilities as well as the success in the process of maximizing assets to meet complex liabilities such that it will help increase profitability. The current tab starts by obtaining, as general inputs, the bank’s regulatory capital obtained earlier from the credit risk models. In addition, the number of trading days in the calendar year of the analysis (e.g., typically between 250 and 253 days), the local currency’s name (e.g., U.S. Dollar or Argentinian Peso), the current period when the analysis is performed and results reported to the regulatory agencies (e.g., January 2015), the number of VaR percentiles to run (e.g., 99.00%), number of scenarios to run and their respective basis point sensitivities (e.g., 100, 200, and 300 basis points, where every 100 basis points represent 1%), and number of foreign currencies in the bank’s investment portfolio. As usual, the inputs, settings, and results can be saved for future retrieval. Figure 1.6 further illustrates the PEAT utility’s ALM-CMOL module for Asset Liability Management. The tab is specifically for Interest Rate Sensitive Assets and Liabilities data where historical impacts of interest-rate sensitive assets and liabilities, as well as foreign currency–denominated assets and liabilities are entered, copied and pasted, or uploaded from a database. Historical Interest Rate data is uploaded where the rows of periodic historical interest rates of local and foreign currencies can be entered, copied and pasted, or uploaded from a database.

Figure 1.6: Asset Liability Management—Interest Rate Risk (Asset and Liability Data)