File Name: Exotic Options – Two Correlated Assets

Location: Modeling Toolkit | Exotic Options | Two Asset Correlated

Brief Description: Computes the value of an option that depends on two assets: a benchmark asset that determines if the option is in the money and a second asset that determines the payoff on the option at expiration

Requirements: Modeling Toolkit

Modeling Toolkit Functions Used: MTTwoAssetCorrelationCall, MTTwoAssetCorrelationPut

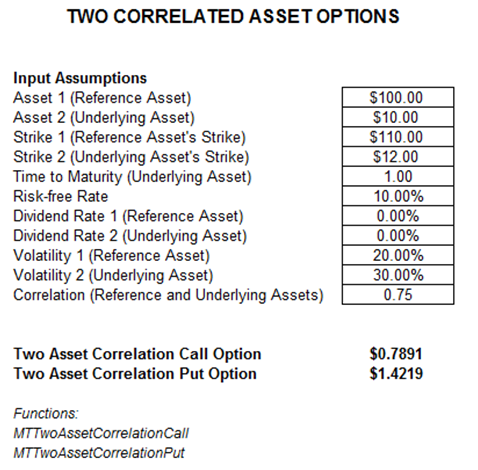

The Two Correlated Asset Options use two underlying assets, Asset 1 and Asset 2 (Figure 77.1). Typically, Asset 1 is the benchmark asset (e.g., a stock index or market comparable stock), whereby if at expiration Asset 1’s values exceed Strike 1’s value, then the option is knocked in the money, meaning that the payoff on the call option is Asset 2 – Strike 2 and Strike 2 – Asset 2 for the put option (for the put, Asset 1 must be less than Strike 1).

A higher positive correlation between the reference and the underlying asset implies that the option value increases as the comovement of both assets is highly positive, meaning that the higher the price movement of the reference asset, the higher the chances of it being in the money and, similarly, the higher the chances of the underlying asset’s payoff being in the money. Negative correlations reduce the option value even if the reference asset is in the money and the value of the option of the underlying is very little in the money or completely out of the money. Correlation is typically restricted between -0.9999 and +0.9999. If there is a perfect correlation (either positive or negative), then there is no point in issuing such an asset, as a regular option model will suffice.

Two Correlated Asset Options sometimes are used as a performance-based payoff option. For instance, the first or reference asset can be a company’s revenues or profit margin; an external index such as the Standard & Poor’s 500; or some reference price in the market such as the price of gold. Therefore, the option is live only if the benchmark value exceeds a prespecified threshold. This European option is exercisable only at expiration. To model an American (exercisable at any time up to and including expiration) or Bermudan option (exercisable at specific periods only, with blackout and vesting periods where the option cannot be exercised), use the Real Options SLS software.

Figure 77.1: Two correlated asset options