File Name: Volatility – Implied Volatility

Location: Modeling Toolkit | Volatility | Implied Volatility

Brief Description: Computes the implied volatilities using an internal optimization routine, given the fair market values of a call or put option as well as all their required inputs

Requirements: Modeling Toolkit, Risk Simulator

Modeling Toolkit Functions Used: MTImpliedVolatilityCall, MTImpliedVolatilityPut

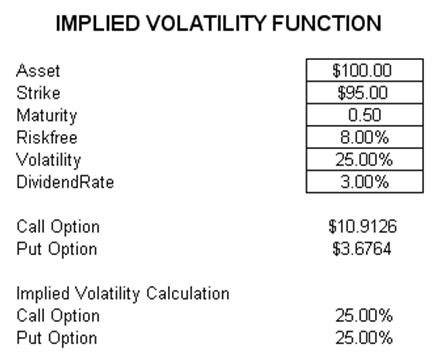

This implied volatility computation is based on an internal iterative optimization, which means it will work under typical conditions (without extreme volatility values, i.e., too small or too large). It is always good modeling technique to recheck the imputed volatility using an options model to make sure the answer coincides before adding more sophistication to the model. That is, given all the inputs in an options analysis as well as the option value, the volatility can be imputed. See Figure 161.1.

Figure 161.1: Getting the implied volatility from options