File Name: Forecasting – Forecasting Manual Computations

Location: Modeling Toolkit | Forecasting | Forecasting Manual Computations

Brief Description: Illustrates how to use Risk Simulator for running optimization to determine the optimal forecasting parameters in several time-series decomposition models

Requirements: Modeling Toolkit, Risk Simulator

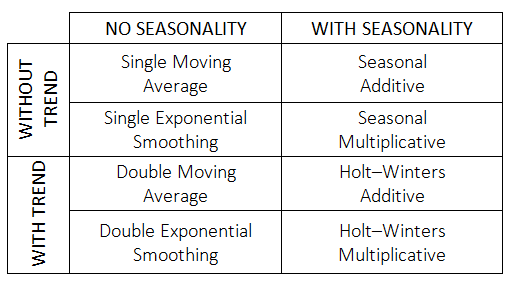

This example model shows the manual computations of the eight time-series decomposition and forecasting techniques in Risk Simulator and how the computations are done. We illustrate the step-by-step computations of backcast and forecast values, plus use Risk Simulator’s optimization routines to find the best and optimal forecast parameters (e.g., Alpha, Beta, and Gamma) that yield the lowest error. The eight methods covered in this model are shown in Figure 83.1.

Figure 83.1: The eight time-series forecasting models

Procedure

The manual computations are shown in each of the worksheets in the model. In some of the methods, optimization is required to find the best input parameters to backcast-fit and forecast-fit the data going forward. In each method requiring optimization (six of the eight methods, excluding the Single Moving Average and Double Moving Average approaches), a new profile has already been created and the relevant objectives and decision variables have been set up. To run the model, follow these steps:

- Go to the relevant worksheet and change the profile to match the worksheet (Risk Simulator | Change Profile) and find the matching profile for the model.

- You can change the decision variables (Alpha, Beta, and Gamma) in the model to some starting point (e.g., 1) so that you can tell whether anything had changed at the end of the optimization procedure. Then run the optimization (Risk Simulator | Optimization | Run Optimization).

To recreate the optimization, follow these steps instead:

- Go to the relevant worksheet, create a new simulation profile (Risk Simulator | New Profile) and give it a name.

- Select the RMSE or Root Mean Squared Error cell, make it an objective (Risk Simulator | Optimization | Set Objective), and set it to Minimize.

- Select the input parameter one at a time (e.g., Alpha, Beta, or Gamma), make it a decision variable (Risk Simulator | Set Decision), and make it a Continuous Variable between 0 and 1 (the input parameters Alpha, Beta, and Gamma can take values only between 0 and 1, inclusive).

- Run the optimization (Risk Simulator | Optimization | Run Optimization) and choose Static Optimization.