Theory

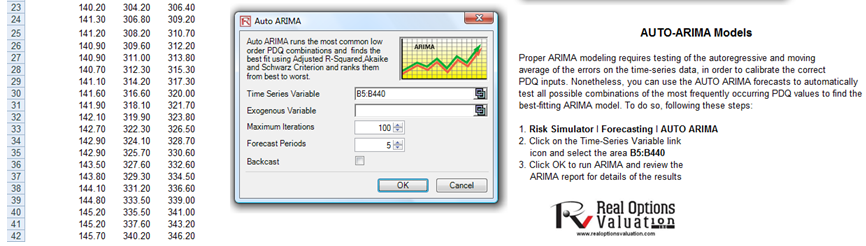

This tool provides analyses identical to the ARIMA module except that the Auto-ARIMA module automates some of the traditional ARIMA modeling by automatically testing multiple permutations of model specifications and returns the best-fitting model. Running the Auto-ARIMA module is similar to running regular ARIMA forecasts. The differences being that the P, D, Q inputs are no longer required and that different combinations of these inputs are automatically run and compared.

Procedure

- Start Excel and enter your data or open an existing worksheet with historical data to forecast (the illustration shown in Figure 11.14 uses the example file located at Risk Simulator | Example Models | 01 Advanced Forecasting Models).

- In the Auto ARIMA worksheet, select Risk Simulator | Forecasting | Auto-ARIMA. You can also access the method through the Forecasting icons ribbon or right-clicking anywhere in the model and selecting the forecasting shortcut menu.

- Click on the link icon and link to the existing time-series data, enter the number of forecast periods desired, and click OK.

ARIMA and AUTO ARIMA Note

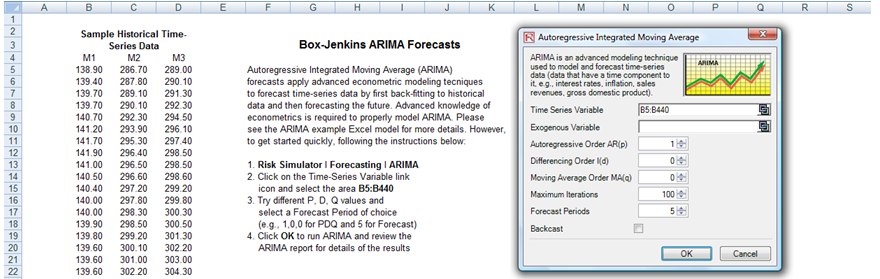

For ARIMA and Auto ARIMA, you can model and forecast future periods either by using only the dependent variable (Y), that is, the Time Series Variable by itself, or you can insert additional exogenous variables (X1, X2,…, Xn) just as in a regression analysis where you have multiple independent variables. You can run as many forecast periods as you wish if you only use the time-series variable (Y). However, if you add exogenous variables (X), be sure to note that your forecast periods are limited to the number of exogenous variables’ data periods minus the time-series variable’s data periods. For example, you can only forecast up to 5 periods if you have time-series historical data of 100 periods and only if you have exogenous variables of 105 periods (100 historical periods to match the time-series variable and 5 additional future periods of independent exogenous variables to forecast the time-series dependent variable).

Figure 11.14: AUTO-ARIMA Module