File Name: Yield Curve – Curve Interpolation BIM

Location: Modeling Toolkit | Yield Curve | Curve Interpolation BIM

Brief Description: Estimates and models the term structure of interest rates and yield curve approximation using a curve interpolation method

Requirements: Modeling Toolkit, Risk Simulator

Modeling Toolkit Function Used: MTYieldCurveBIM

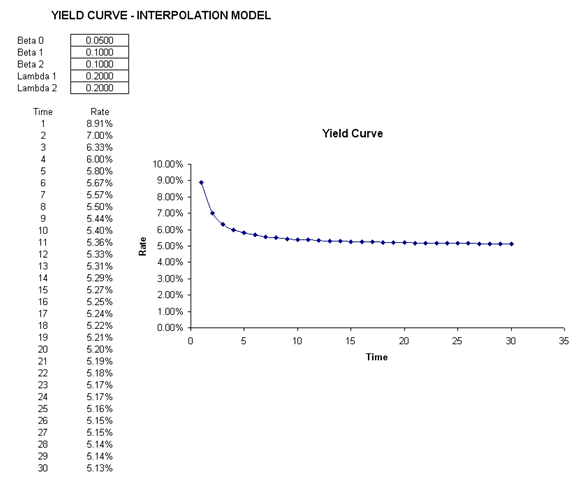

A number of alternative methods exist for estimating the term structure of interest rates and the yield curve. Some are fully specified stochastic term structure models while others are simply interpolation models. The former include the CIR and Vasicek models (illustrated in other chapters in this book), while the latter are interpolation models such as the Bliss or Nelson approach. This chapter looks at the Bliss Interpolation model (BIM) (Figure 164.1) for generating the term structure of interest rates and yield curve estimation. Some econometric modeling techniques are required to calibrate the values of several input parameters in this model. The Bliss approach modifies the Nelson-Siegel method by adding an additional generalized parameter. Virtually any yield curve shape can be interpolated using these models, which are widely used at banks around the world.

Figure 164.1: BIM model