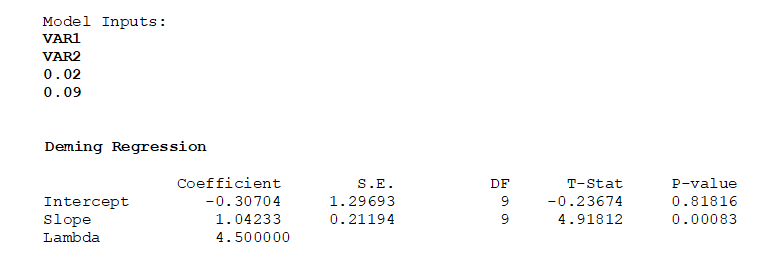

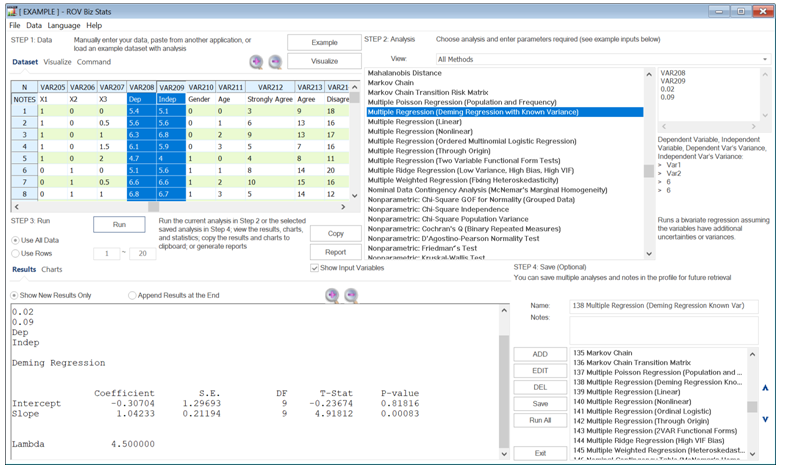

In regular multivariate regressions, the dependent variable is modeled and predicted by independent variables ![]() with some error ε. However, in a Deming regression, we further assume that the data collected for the variables have additional uncertainties and errors, or variances, that are used to provide a more relaxed fit in a Deming model. This implies that the predicted values will have a higher level of variance and uncertainty. The estimated variances are used to determine the lambda, where

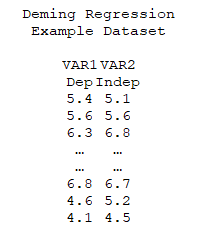

with some error ε. However, in a Deming regression, we further assume that the data collected for the variables have additional uncertainties and errors, or variances, that are used to provide a more relaxed fit in a Deming model. This implies that the predicted values will have a higher level of variance and uncertainty. The estimated variances are used to determine the lambda, where ![]() and this parameter is minimized to determine the value of the slope and intercept coefficients. The optimized coefficients will be unbiased estimators of the true population parameters, and the error residuals are assumed to be normally distributed. The following illustrates a sample dataset needed when using BizStats to compute a Deming regression, as well as the required input parameters. This bivariate model requires the dependent and independent variables, followed by the known variance for both variables.

and this parameter is minimized to determine the value of the slope and intercept coefficients. The optimized coefficients will be unbiased estimators of the true population parameters, and the error residuals are assumed to be normally distributed. The following illustrates a sample dataset needed when using BizStats to compute a Deming regression, as well as the required input parameters. This bivariate model requires the dependent and independent variables, followed by the known variance for both variables.