File Name: Risk Hedging – Effects of Fixed versus Floating Rates

Location: Modeling Toolkit | Risk Hedging | Effects of Fixed versus Floating Rates

Brief Description: Sets up various levels of hedging to determine the impact on earnings per share

Requirements: Modeling Toolkit

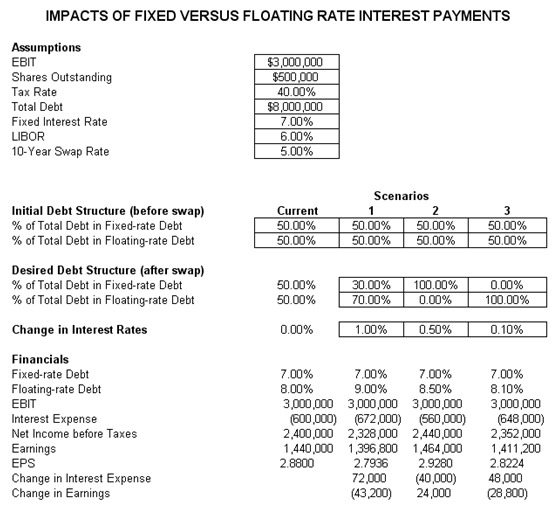

This model illustrates the impact on financial earnings and earnings before interest and taxes (EBIT) of a hedged versus unhedged position. The hedge is done through interest rate swap payments. Various scenarios of swaps (different combinations of fixed rate versus floating rate debt) can be generated and tested in this model to determine the impact to earnings per share (EPS) and other financial metrics. See Figure 126.1. The foreign exchange cash flow hedge model shown in the next chapter goes into more detail on the hedging aspects of foreign exchange through the use of risk simulation.

This model looks at several scenarios of changes in interest rates (row 23 in the model), where a fixed rate versus a floating rate is applied (rows 26 and 27) based on the proportion of fixed to floating debt structure (rows 16 and 17). The fixed rate is fixed under all conditions whereas the floating rate is pegged to the LIBOR rate and some predetermined swap rate (where a floating is swapped with a fixed rate and vice versa) as well as the changes to the prevailing interest rate in the economy. For example, the floating rate will be equal to the fixed rate adjusted for the swap rate plus LIBOR and changes to the prevailing market rate (see row 27 of the model).

This model can then be simulated by adding assumptions to the LIBOR and change in the prevailing interest rates, to determine the probabilistic impacts to changes in the company’s earnings based on a fixed versus floating rate regime.

Figure 126.1: Impacts of an unhedged versus hedged position