A Multiple Weighted regression runs a Multivariate Regression on Weighted Variables (also known as weighted least squares, or WLS) to correct for heteroskedasticity in all the variables. The weights used to adjust these variables are the user input standard deviations. As mentioned, the standard OLS approach minimizes the sum of squares of the errors![]() but in a weighted least squares approach, we add an additional weight variable

but in a weighted least squares approach, we add an additional weight variable ![]() such that we have

such that we have![]() Similarly, in matrix notation, the standard regression’s

Similarly, in matrix notation, the standard regression’s![]() These weights are used as an additional input variable to the model in situations where the errors are heteroskedastic.

These weights are used as an additional input variable to the model in situations where the errors are heteroskedastic.

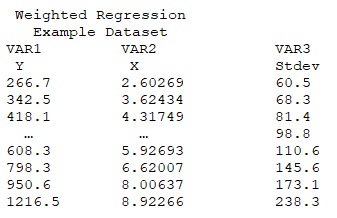

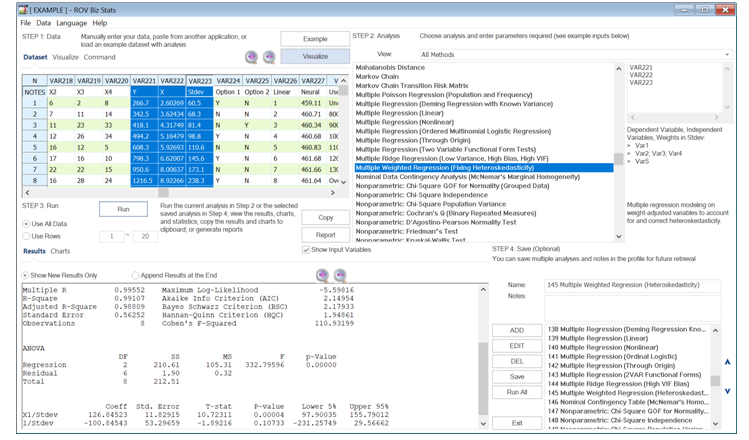

The following provides an example dataset and results from BizStats using a weighted regression model. Notice that a new input variable called standard deviation is required.

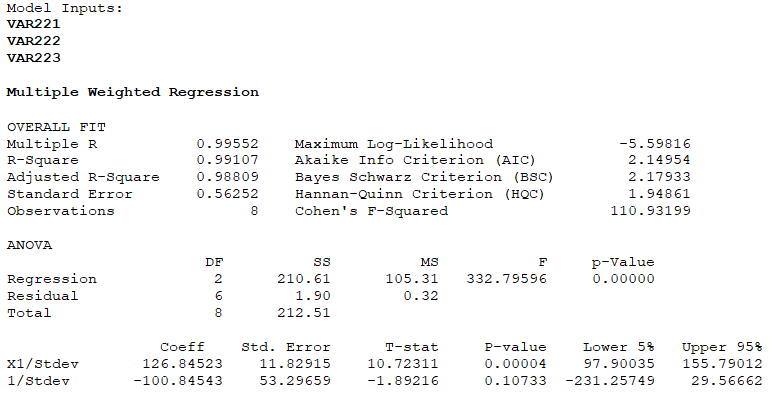

Finally, the regression results will show 1/Stdev as a representation of the weighted intercept and X/Stdev as a representation of the weighted X variable. These variables can be used exactly as in a standard regression model to determine the predicted dependent variable’s values. In fact, the results from a WLS should be relatively close to those in an OLS model.