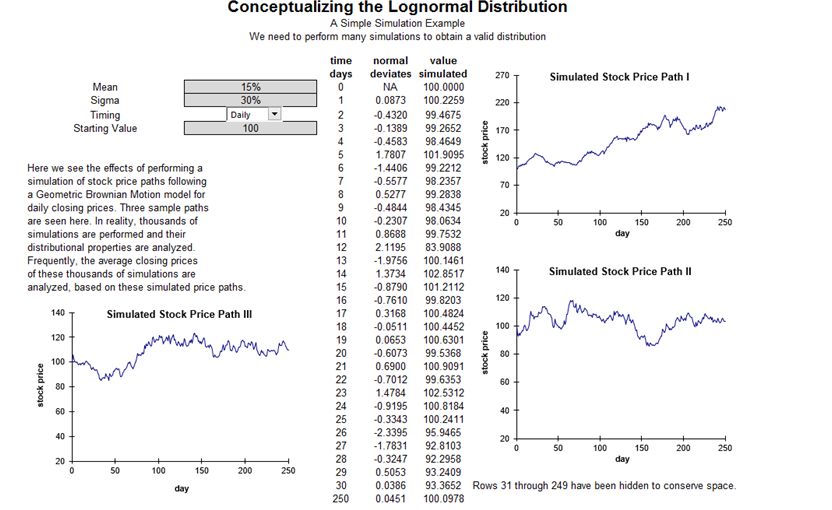

Figure 13.3 illustrates some traditional approaches used to deal with uncertainty and risk. The methods include performing sensitivity analysis, scenario analysis, and probabilistic scenarios. The next step is the application of Monte Carlo simulation, which can be seen as an extension to the next step in uncertainty and risk analysis. Figure 13.4 shows a more advanced use of Monte Carlo simulation for forecasting. The examples in Figure 13.4 show how Monte Carlo simulation can be really complicated depending on its use. The Risk Simulator software has a stochastic process module that applies some of these more complex stochastic forecasting models, including Brownian motion, mean-reversion, and random walk models.

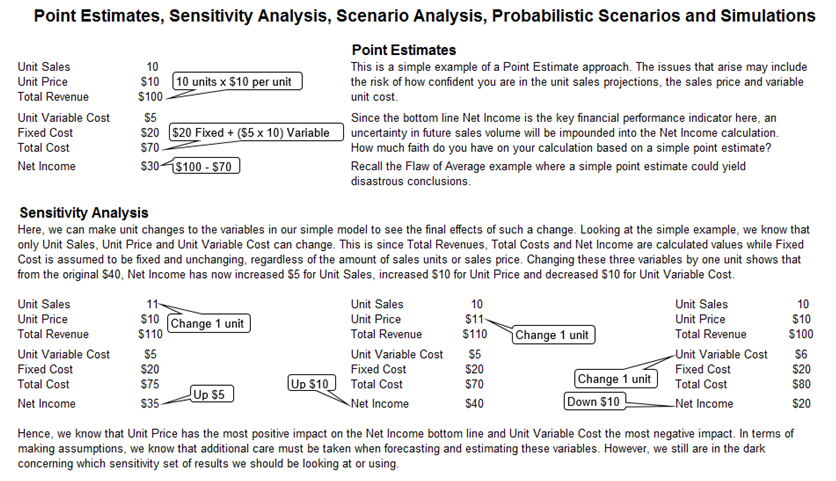

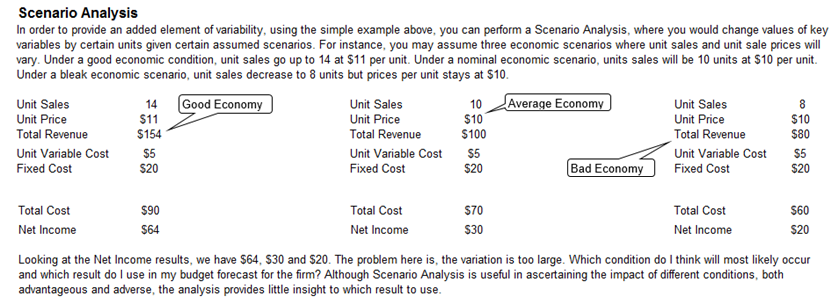

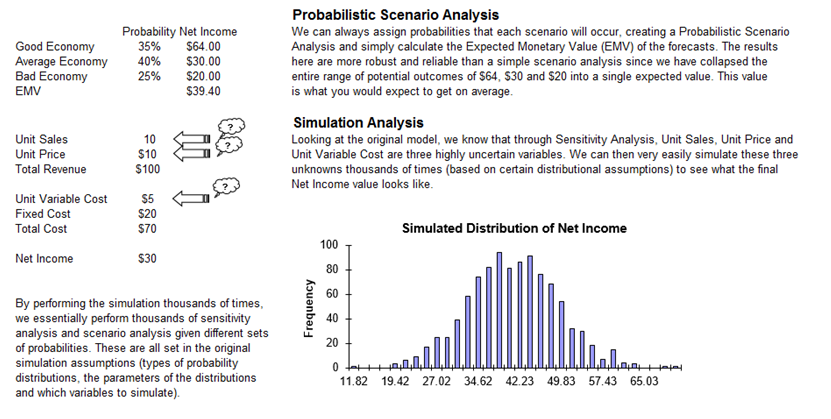

Figure 13.3: Point Estimates, Sensitivity Analysis, Scenario Analysis, and Simulations

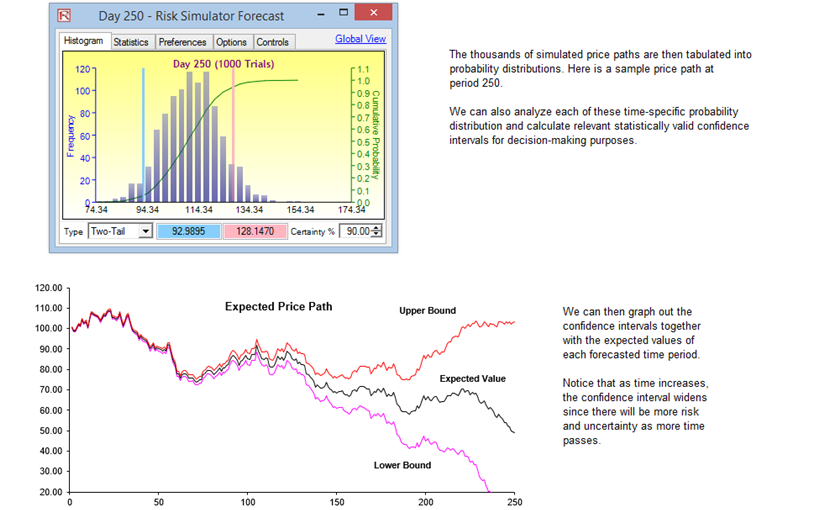

Figure 13.4: Conceptualizing the Lognormal Distribution