File Name: Value at Risk – Static Covariance Method

Location: Modeling Toolkit | Value at Risk | Static Covariance Method

Brief Description: Computes a static Value at Risk (VaR) using a correlation and covariance method, to obtain the portfolio’s VaR after accounting for the individual component’s returns, volatility, cross-correlations, holding period, and VaR percentile

Requirements: Modeling Toolkit, Risk Simulator

Modeling Toolkit Function Used: MTVaRCorrelationMethod

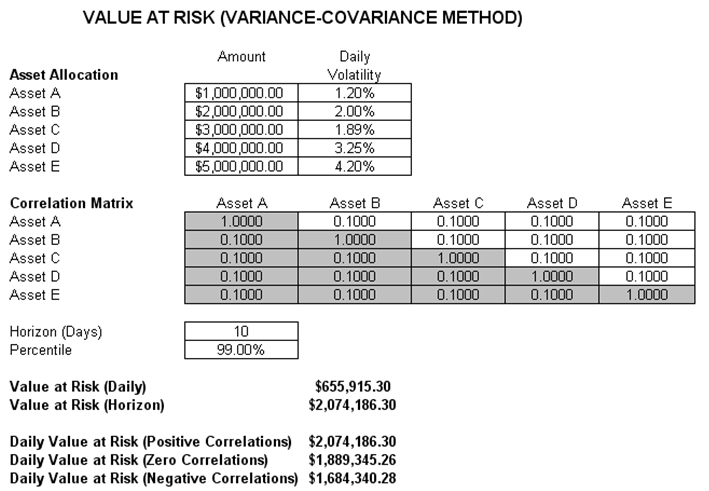

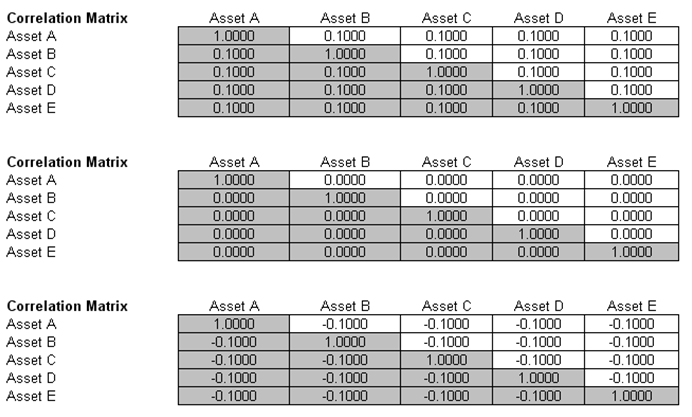

This model is used to compute the portfolio’s Value at Risk (VaR) at a given percentile for a specific holding period, after accounting for the cross-correlation effects between the assets (Figure 160.1). The daily volatility is the annualized volatility divided by the square root of trading days per year. Typically, positive correlations tend to carry a higher VaR compared to zero correlation asset mixes, whereas negative correlations reduce the total risk of the portfolio through the diversification effect (Figure 160.2). The approach used is a portfolio VaR with correlated inputs, where the portfolio has multiple asset holdings with different amounts and volatilities. Each asset is also correlated to each other. The covariance or correlation structural model is used to compute the VaR given a holding period or horizon and percentile value (typically 10 days at 99% confidence).

Figure 160.1: Computing Value at Risk using the covariance method

Figure 160.2: Value at Risk results with different correlation levels