File Name: Debt Analysis – Vasicek Price and Yield of Risky Debt

Location: Modeling Toolkit | Debt Analysis | Vasicek Price and Yield of Risky Debt

Brief Description: Uses the Vasicek model to price risky debt and to compute the yield on risky debt, where the underlying interest rate structure is stochastic, volatile, and mean-reverting (this model is also often used to compute and forecast yield curves)

Requirements: Modeling Toolkit, Risk Simulator

Modeling Toolkit Functions Used: MTBondVasicekBondPrice, MTBondVasicekBondYield

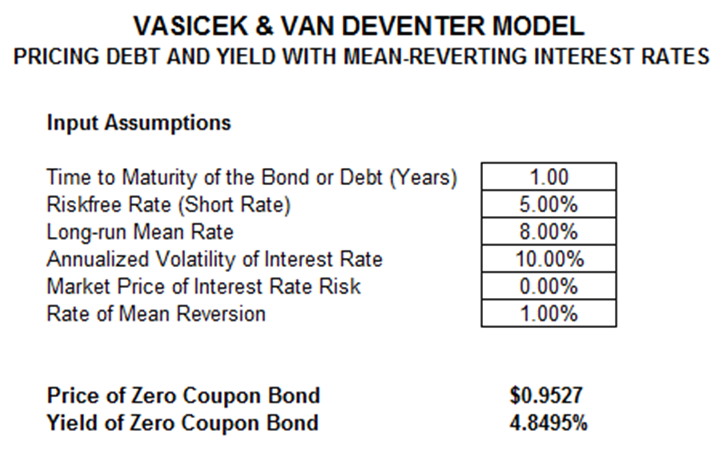

The Vasicek stochastic model of mean-reverting interest rates is modeled here to determine the value of a zero-coupon bond (Figure 22.1) as well as reconstructing the term structure of interest rates and interest rate yield curve. This model assumes a mean-reverting term structure of interest rates with a rate of reversion as well as a long-run rate that the interest reverts to in time. Use the Yield Curve Vasicek model to generate the yield curve and term structure of interest rates using this model. You may also use Risk Simulator to run simulations on the inputs to determine the price and yield of the zero-coupon debt, or to determine the input parameters such as the long-run mean rate and rate of mean reversion (use Risk Simulator’s Statistical Analysis tool to determine these values based on historical data).

The previous chapter uses a modification of this Vasicek model to price debt call and put options, versus the models described in this chapter that are used for pricing the risky bond and yield on the bond based on stochastic and mean-reverting interest rates. If multiple maturities and their respective input parameters are obtained, the entire term structure of interest rates and yield curve can be constructed, where the underlying processes of these rates are assumed to be mean reverting.

Figure 22.1: Price and yield of risky debt