File Name: Value at Risk – Portfolio Operational and Capital Adequacy

Location: Modeling Toolkit | Value at Risk | Portfolio Operational and Capital Adequacy

Brief Description: Illustrates how to use Risk Simulator for distributional fitting, to find the best-fitting distributions for credit risk and operational risk parameters, and how to run Monte Carlo simulation on these credit and operational risk variables to determine the total capital required under a 99.50% Value at Risk

Requirements: Modeling Toolkit, Risk Simulator

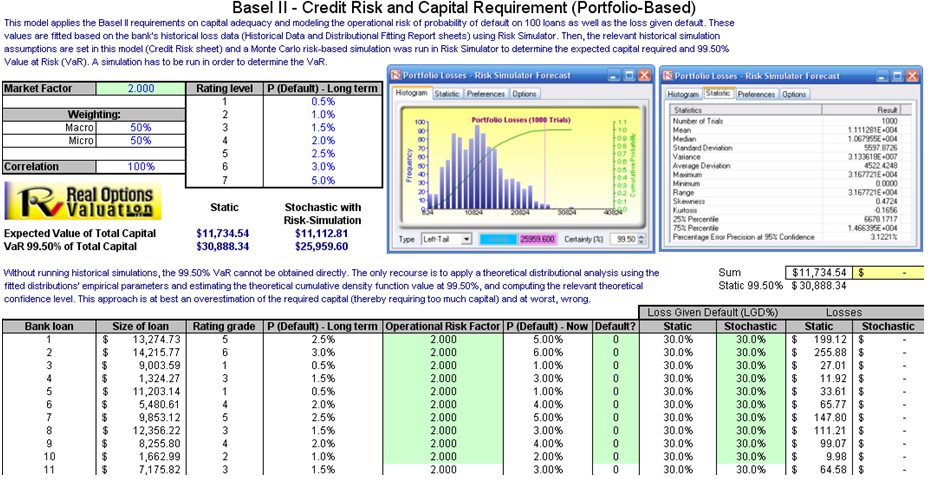

This model shows how operational risk and credit risk parameters are fitted to statistical distributions and their resulting distributions are modeled in a portfolio of liabilities to determine the Value at Risk (VaR) 99.50th percentile certainty for the capital requirement under Basel III/IV/IV requirements. It is assumed that the historical data of the operational risk impacts (Historical Data worksheet) are obtained through econometric modeling of the Key Risk Indicators.

The Distributional Fitting Report worksheet is a result of running a distributional fitting routine in Risk Simulator to obtain the appropriate distribution for the operational risk parameter. Using the resulting distributional parameter, we model each liability’s capital requirements within an entire portfolio. Correlations can also be inputted if required, between pairs of liabilities or business units. The resulting Monte Carlo simulation results show the VaR capital requirements. Note that an appropriate empirically based historical VaR cannot be obtained if distributional fitting and risk-based simulations were not first run. Only by running simulations will the VaR be obtained.

Procedure

To perform distributional fitting, follow the steps below:

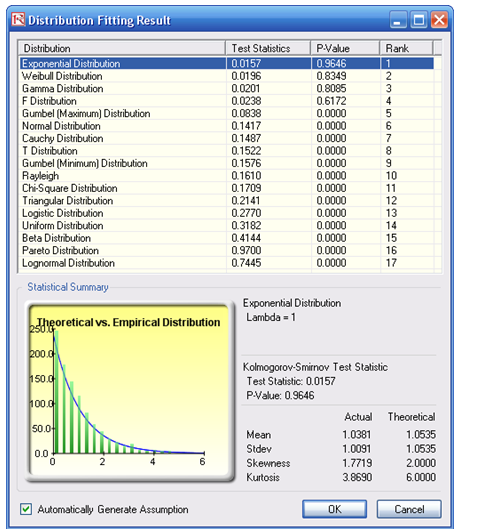

- In the Historical Data worksheet (Figure 3.12), select the data area (cells C5:L104) and click on Risk Simulator | Analytical Tools | Distributional Fitting (Single Variable).

- Browse through the fitted distributions and select the best-fitting distribution (in this case, the exponential distribution in Figure 3.13) and click OK.

Figure 3.12: Sample Historical Bank Loans

Figure 3.13: Data Fitting Results

To run a simulation in the portfolio model:

- You may now set the assumptions on the Operational Risk Factors with the exponential distribution (fitted results show Lambda = 1) in the Credit Risk Note that the assumptions have been set for you in advance. You may set them by going to cell F27 and clicking on Risk Simulator | Set Input Assumption, selecting Exponential distribution and entering 1 for the Lambda value, and clicking OK. Continue this process for the remaining cells in column F or simply perform a Risk Simulator Copy and Risk Simulator Paste on the remaining cells:

- Note that since the cells in column F have assumptions set, you will first have to clear them if you wish to reset and copy/paste parameters. You can do so by first selecting cells F28:F126 and clicking on the Remove Parameter icon or selecting Risk Simulator | Remove Parameter.

- Then select cell F27, click on the Risk Simulator Copy icon or select Risk Simulator | Copy Parameter, and then select cells F28:F126 and click on the Risk Simulator Paste icon or select Risk Simulator | Paste Parameter.

- Next, additional assumptions can be set such as the probability of default using the Bernoulli distribution (column H) and Loss Given Default (column J). Repeat the procedure in Step 3 if you wish to reset the assumptions.

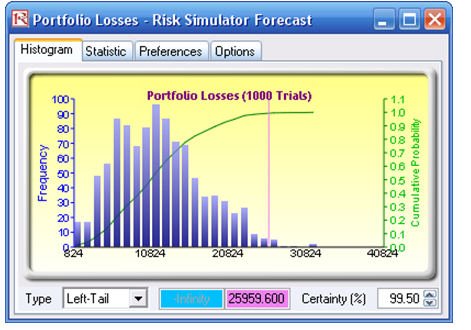

- Run the simulation by clicking on the RUN icon or clicking on Risk Simulator | Run Simulation.

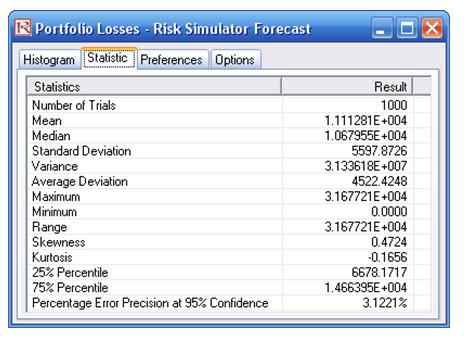

- Obtain the Value at Risk by going to the forecast chart once the simulation is done running and selecting Left-Tail and typing in 99.50. Hit TAB on the keyboard to enter the confidence value and obtain the VaR of $25,959 (Figure 3.14).

Figure 3.14: Simulated Forecast Results